Bankroll Management for Horse Racing: Staking Plans, Unit Sizing and How to Protect Your Betting Bank

Table of Contents

- Why Most Beginners Lose — and How a Staking Plan Fixes It

- Setting Your First Betting Bank: How Much Is Enough

- Flat Stakes vs Percentage Staking vs Level-Stakes to Profit

- Unit Sizing: The 1–2% Rule Explained

- Why Psychology Matters More Than Strategy

- Tracking Your Bets: What to Record and Why

- Frequently Asked Questions

Why Most Beginners Lose — and How a Staking Plan Fixes It

I lost my entire first betting bank in eleven days. Not because I picked bad horses — three of my first five bets won. I lost it because I had no plan for how much to stake, no system for when to stop, and no understanding of why a 30 pound win on Saturday led to a 50 pound loss on Monday. The problem wasn’t selection. The problem was money management, and it’s the gap that separates punters who survive from punters who quit.

42% of UK bettors describe their experience as positive. Another 35% rate it as neutral. The remaining 23% — the ones who find it negative — disproportionately share one trait: they don’t manage their money. They stake too much on individual bets, increase stakes after wins, chase losses after defeats, and treat their betting bank as an emotional piggy bank rather than a strategic resource. Every one of those behaviours is fixable with a simple staking plan.

This guide covers how to set a betting bank, how to size your bets, and how to choose a staking plan that matches your goals. I’ll keep the maths accessible and the advice practical. Nothing here requires a spreadsheet or a finance degree — just discipline and a willingness to treat your betting money as something worth protecting.

If you’ve already read the beginner’s guide to placing your first bet, you know the basics of how racing works. This article picks up where that one touches on bankroll — here, we go deep. Because the truth is, the difference between a punter who lasts six months and one who lasts six years almost never comes down to which horses they pick. It comes down to how they manage the money behind those picks.

Setting Your First Betting Bank: How Much Is Enough

Your betting bank is not your savings account. It’s not your rent money. It’s not the cash in your current account. It’s a separate, ring-fenced amount that you can lose entirely without any impact on your life. If that amount is 50 pounds, your bank is 50 pounds. If it’s 500 pounds, fine. The number matters less than the separation.

Since February 2025, the UK Gambling Commission’s affordability framework triggers soft checks at 150 pounds in net monthly deposits. This isn’t a limit on how much you can bet — it’s a threshold beyond which operators may use data sources to assess financial vulnerability. For most beginners, staying comfortably below that number is both practically wise and strategically sound. A 100 pound bank, replenished monthly if needed, gives you enough to bet meaningfully without approaching the check threshold.

The amount should reflect your intentions. If you plan to bet on a couple of races per week, 50 to 100 pounds provides enough for 25 to 50 bets at 2 pound stakes — roughly six months of activity if you’re disciplined. If you plan to bet daily across multiple meetings, you’ll need more capital to withstand the natural variance in results. What you shouldn’t do is start with an amount you’ve calculated backwards from the returns you hope to make. “I want to win 500 pounds a month, so I need a 1,000 pound bank” is backwards logic. You don’t control returns. You control risk.

Once the bank is set, the cardinal rule is simple: when it’s gone, it’s gone. You can choose to replenish it next month or next quarter, but you never top it up mid-session to chase a loss. That boundary — between planned bankroll and emergency injection — is where most beginners’ discipline breaks down. Set the bank, write the number down, and treat it as a budget, not a starting point for negotiation.

A note on the affordability landscape: Grainne Hurst of the Betting and Gaming Council has argued that requiring punters to hand over bank statements is intrusive and risks driving customers to the unregulated market. Whether or not you agree with that position, the practical reality is that staying within your means — which a properly sized bank ensures — keeps your betting experience friction-free. Nobody who bets within a sensible bankroll triggers enhanced checks, and nobody who triggers enhanced checks was likely betting within their means. The two things are self-reinforcing.

Flat Stakes vs Percentage Staking vs Level-Stakes to Profit

Three years into my betting career, I kept meticulous records of my selections but had zero consistency in what I staked. A horse I loved got 10 pounds. One I quite liked got 5. A hunch got 20. My strike rate was 22% — respectable for the prices I was backing — but my P&L was negative because I was putting the biggest stakes on the worst-justified selections. A staking plan fixed that within a month.

Flat staking is the simplest approach. Every bet, regardless of odds or confidence, receives the same stake. If your unit is 2 pounds, every bet is 2 pounds. The advantage is total discipline — you can’t talk yourself into a bigger stake on a “certainty” that turns out to be anything but. The disadvantage is that it ignores information. If you genuinely have more confidence in one selection than another, flat staking treats them identically.

I started with flat staking and still believe it’s the best system for the first six months of serious betting. It removes emotion from the equation entirely. When every bet costs the same, your focus shifts to selection quality rather than stake manipulation, and that focus is where the real skill develops.

Percentage staking adjusts each bet to a fixed percentage of your current bank. If your bank is 200 pounds and your percentage is 2%, each bet is 4 pounds. If the bank grows to 250 pounds, bets become 5 pounds. If it shrinks to 150 pounds, bets drop to 3 pounds. The system is self-correcting: winning streaks increase stakes gradually, losing streaks reduce them, and the risk of ruin — losing your entire bank — is mathematically very low.

The drawback of percentage staking is that it requires recalculating before every bet. In practice, I round to the nearest pound and recalculate daily rather than per bet. The precision isn’t important; the principle is. Your exposure scales with your resources, which means a bad week reduces your future risk automatically.

Level-stakes to profit (sometimes called “target staking”) adjusts the stake so that every winning bet returns the same profit amount. If your target profit is 10 pounds and the horse is 4/1, you stake 2.50 pounds. If the horse is 2/1, you stake 5 pounds. The logic is that your profit per winner is constant, regardless of odds. The problem: it puts larger stakes on shorter-priced horses, which means heavier losses when favourites get beaten. I used this system for a year and found that the psychological comfort of consistent winnings was offset by the discomfort of larger individual losses. It suits patient, methodical bettors who back a narrow range of odds.

No staking plan turns a losing selection strategy into a profitable one. The plan manages risk and prevents catastrophic loss — it doesn’t generate returns by itself. Think of it as the chassis of a car: it doesn’t make the engine faster, but without it the engine is useless.

Which plan should you choose? If you’re in your first year of serious betting, start with flat staking. It eliminates the most common mistake — oversizing bets when emotions are high — and gives you clean data to analyse. After a year, if your records show consistent positive selection and you want to scale with your bank, move to percentage staking. Level-stakes to profit is a specialist tool for punters who back within a narrow odds band and have a proven long-term edge. It’s not a beginner’s system, despite how intuitive it sounds.

Unit Sizing: The 1–2% Rule Explained

Whatever staking plan you choose, the unit size needs to be small enough that a losing streak doesn’t wipe you out and large enough that a winning bet feels worth the effort. The standard recommendation is 1 to 2% of your total bank per bet. On a 200 pound bank, that’s 2 to 4 pounds per bet.

Here’s why that range works. Horse racing has a natural variance that even the best punters can’t avoid. A strike rate of 20% — one winner in five — means you’ll regularly experience runs of 10, 15, even 20 consecutive losers. It’s not bad luck; it’s probability. At 2% per bet on a 200 pound bank (4 pounds per bet), a 20-bet losing streak costs 80 pounds. Painful, but you still have 120 pounds to recover with. At 10% per bet (20 pounds), the same losing streak costs 200 pounds — your entire bank, gone.

I’ve tested various unit sizes over thousands of bets and settled on 1.5% as my standard for flat staking, with the option to go to 2.5% on bets where my analysis is strongest. That slight variation introduces a confidence-weighting mechanism without the wild swings that larger adjustments create. The key is that even my “strong” bet is only 67% larger than my standard bet, not three or four times bigger.

For beginners, I’d recommend starting at a flat 2% — no variation, no confidence ratings, no exceptions. Stick with that for at least 100 bets. By that point, you’ll have enough data to know your strike rate, your average odds, and whether your staking needs adjusting. Changing your unit size before you have 100 bets of data is optimising in the dark.

A practical example of what 2% looks like in action. You start with a 200 pound bank. Your unit is 4 pounds. You place 10 bets in the first week: 2 winners at 5/1 and 4/1, 8 losers. The 2 winners return 24 and 20 pounds respectively. Total return: 44 pounds. Total staked: 40 pounds. Net profit for the week: 4 pounds. Your bank is now 204 pounds. Under flat staking, your unit stays at 4 pounds. Under percentage staking, your unit creeps up to 4.08 pounds — round it to 4 and move on.

Week two: 1 winner at 3/1 from 8 bets. Return: 16 pounds. Staked: 32 pounds. Net loss: 16 pounds. Bank drops to 188 pounds. Under percentage staking, your unit drops to 3.76 pounds — round to 3.75 or 4, either works. The point is the system self-adjusts. You’re never overexposed relative to your current position.

The temptation that kills most beginners at this stage is the thought: “I’m only betting 4 pounds. Even if I win at 5/1, that’s only 20 pounds profit. That’s not worth the effort of all this analysis.” It is. Twenty pounds profit from a 4 pound risk is a 500% return on that individual bet. The problem isn’t the return — it’s the expectation. If you came to horse racing hoping to turn 200 pounds into 2,000 pounds in a month, no staking plan will satisfy you, and no staking plan should. The goal of bankroll management is survival and gradual growth, not transformation.

Why Psychology Matters More Than Strategy

The staking plan protects your bank from mathematical risk. Nothing protects it from you. Every punter I know — myself included — has at some point overridden their own rules because a feeling was too strong to ignore. The feeling is usually wrong.

Chasing losses is the most destructive behaviour in betting. You lose 20 pounds in the afternoon, so you bet 30 pounds on the evening card to “get it back.” The evening selection was never part of your plan — it’s a reaction to a loss, not a response to an opportunity. Even if the horse wins, you’ve established a pattern that will eventually destroy your bank. The loss you’re chasing was already within your plan’s tolerance. The recovery bet was not.

The inverse trap is equally dangerous: increasing stakes after a winning run because you feel invincible. Three winners in a row creates a sense of momentum, as if you’ve cracked a code. You haven’t. Each bet is independent. The third winner doesn’t make the fourth more likely. If anything, the overconfidence that follows a streak leads to sloppier analysis and worse selections — exactly when you’re putting up the biggest stakes. The pattern is predictable and repeatable: win, win, win, increase stake, lose big, spiral.

The Betting and Gaming Council’s chief executive Grainne Hurst has noted that the vast majority of customers bet safely and within their means. That’s true statistically, but “within their means” and “within a plan” aren’t the same thing. You can afford to lose 200 pounds and still lose it in a way that teaches you nothing and provides no path to improvement. A plan converts affordable loss into structured learning. Without it, you’re just spending money on random outcomes. I’ve written a full guide to the cognitive biases that undermine even well-intentioned punters — it’s worth reading alongside this piece if you want to understand why discipline breaks down and how to rebuild it.

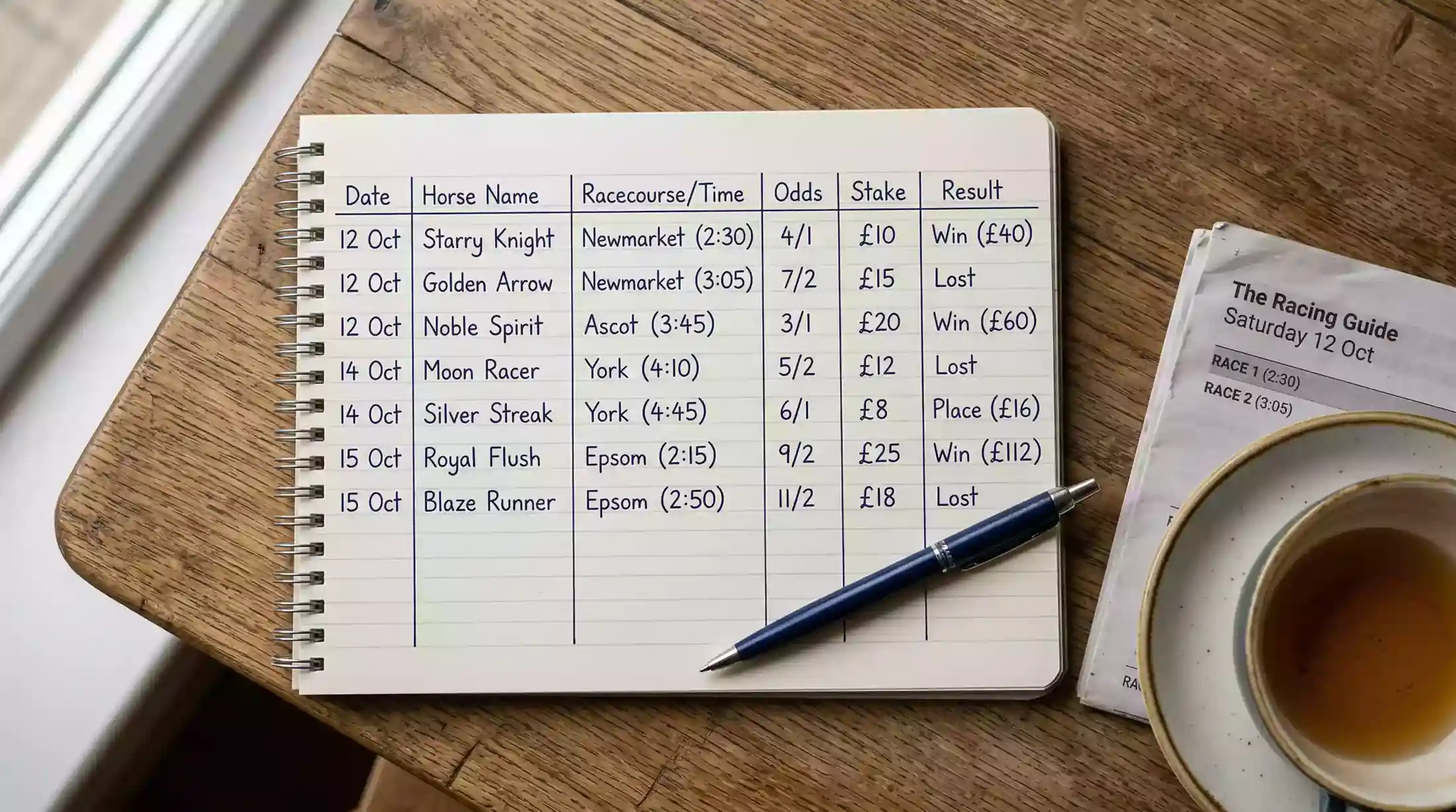

Tracking Your Bets: What to Record and Why

7% of UK adults bet on horse racing during the festival season between April and July. Outside of that window, participation drops to around 4%. Those seasonal patterns mean your own betting rhythm will shift throughout the year, and without records, you’ll have no way of knowing whether your approach is working across different conditions.

At minimum, track these fields for every bet: date, race, horse, odds taken, stake, bet type, result, and return. That’s eight columns in a spreadsheet or a simple notes app. From those eight fields, you can calculate your strike rate (winners divided by total bets), your profit or loss by week and month, your average odds, your return on investment (profit divided by total stakes), and your longest losing streak.

The losing streak number is the most important one for bankroll management. If your records show that your longest losing run is 14 bets, you know your unit size needs to accommodate at least a 20-bet streak (always build in a margin). At 2% per bet, a 20-bet streak costs 40% of your bank. At 5%, it costs 100%. The records tell you whether your unit sizing is appropriate for your actual results, not your theoretical ones.

I review my records every Sunday evening. It takes ten minutes. I look at the week’s strike rate, the total staked versus returned, and any bets where I deviated from my staking plan. Those deviations are almost always the worst-performing bets of the week — confirmation, week after week, that the plan works better than my instincts. That weekly review is the closest thing to a free edge in betting: it costs nothing, takes minimal time, and consistently improves decision-making.

After six months of records, you’ll have something no tipster or betting guide can give you: a personalised dataset of your own betting behaviour. You’ll know which race types you’re best at, which odds ranges are most profitable for you, which days of the week you make your worst decisions (Saturday afternoon, in my case), and whether your staking plan needs refinement. Data replaces guesswork, and guesswork is what loses most punters their money.

One pattern my own records revealed surprised me: my win-only bets in National Hunt handicaps at odds of 6/1 to 10/1 consistently outperformed every other category. Flat maidens, which I thought I understood well, were a consistent drain. Without the records, I’d have continued splitting my attention evenly. With them, I reallocated time and stakes to the category where I had a demonstrable edge. That single adjustment improved my annual ROI by several percentage points — not because I suddenly became a better analyst, but because I stopped wasting effort on areas where I wasn’t one.

Frequently Asked Questions

What percentage of my bankroll should each bet be?

Between 1% and 2% of your total bank per bet is the standard recommendation. On a 200 pound bank, that means individual bets of 2 to 4 pounds. This range ensures you can withstand natural losing streaks without depleting your bank. Start at a flat 2% and adjust only after collecting data from at least 100 bets.

Should I increase my stakes after a winning streak?

Only if you are using percentage staking, where the increase happens automatically because your bank has grown. Never increase stakes manually because you feel confident after a run of winners. Winning streaks end, and inflated stakes on the final losing bet can wipe out the gains from the streak itself.

How do I know when to stop betting for the day?

Set a session limit before you start — either a number of bets or a loss amount. A common approach is to stop after three consecutive losses in a day or after losing 5% of your bank in a single session. The specific number matters less than having a predefined rule that removes the decision from the moment.

What is a realistic win rate for a horse racing beginner?

Most recreational bettors who do basic form analysis achieve a strike rate of 15 to 20% on selections at average odds of 4/1 to 6/1. That range typically produces a small negative return overall, with the goal being to improve selection quality over time. A consistent 20% strike rate at average odds of 5/1 would be marginally profitable after the bookmaker’s margin.

Created by the ”First bet Horse Racing” editorial team.